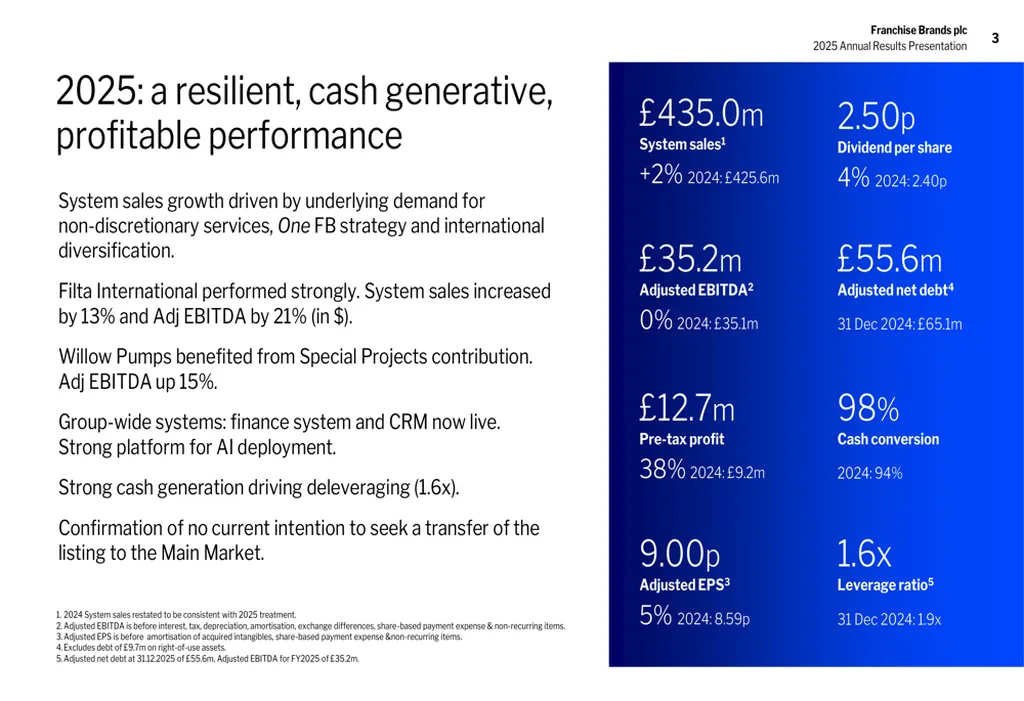

The shift at Franchise Brands PLC from an acquisitive growth model to one centred on operational leverage and capital returns marks a significant inflection point for the franchise water and waste services sector. The 15% reduction in adjusted net debt to £55.6 million, coupled with a leverage ratio of 1.6x, signals a deliberate pivot toward financial discipline rather than expansion at any cost. This deleveraging trajectory, guided by a board that has ruled out major acquisitions until at least 2028, reframes what success looks like in water utility franchising—not through volume of acquisitions, but through cash flow optimisation and margin consistency.

The Water & Waste Services division, anchored by Metro Rod, Metro Plumb, and Willow Pumps, delivered £11.8 million in adjusted EBITDA, yet its growth story remains uneven. While management points to opportunities in housing associations and food manufacturing, the division’s expansion potential is constrained by regional market conditions. The UK, contributing 52% of group EBITDA, faces subdued demand, whereas North America and Europe show divergent trajectories—Filta’s U.S. business grew 13% in system sales with EBITDA up 21% in local currency, offsetting softness in Benelux and the UK. This geographic and segment dispersion underscores a critical truth: in water and drainage services, resilience is not uniform. It is earned through diversification across end-markets and customer types.

The introduction of FiltaClean, including the Ceiling Pro offering, suggests a strategic pivot beyond traditional commercial kitchen filtration. This expansion into air and surface cleaning services hints at a broader convergence in facilities maintenance—a trend likely to accelerate as food service operators seek integrated hygiene solutions. For Franchise Brands, this diversification is not just about revenue growth; it’s about reducing exposure to single-sector risk. The company’s portfolio now spans hydraulic hose services, drainage, plumbing, kitchen filtration, and environmental cleaning, positioning it to weather downturns in any one vertical.

Technology, too, is becoming a silent accelerator. The “One Franchise Brands” initiative—rolling out NetSuite, HubSpot, and a unified work management system—is not merely an IT upgrade. It’s a foundation for cross-selling and operational transparency. With franchisees operating dispersed service networks, standardised CRM and work order systems can unlock latent synergies, particularly in scheduling preventive maintenance across multiple brands. The £2.1 million software capitalisation in 2025 is a small price for a platform that could scale EBITDA margins beyond the current 86% before group overheads.

Investor reaction—shares rising 4.86% to £117.44—validates the strategy. The market is rewarding discipline over growth at all costs. Yet the true test lies ahead. Can Franchise Brands sustain cash conversion near 100% while funding organic expansion and returning capital via dividends and buybacks? The progressive dividend policy, with a 4% increase to 2.50 pence per share, sends a clear message: this is a business designed to return cash, not hoard it for the next acquisition.

What this means for the sector is instructive. Franchise models in water and waste services are maturing. The low-hanging fruit of bolt-on acquisitions is thinning, and the focus is shifting to operational excellence, technology integration, and customer diversification. Franchise Brands’ experience suggests that the most sustainable growth is not about buying more brands, but about extracting more value from existing ones.

The message to competitors is equally clear: scale alone is not a moat. Margins, cash conversion, and technology-enabled service integration are becoming the new benchmarks. In an industry where margins can erode quickly under regulatory or competitive pressure, the ability to standardise processes and deepen customer relationships will separate leaders from followers. Franchise Brands’ journey—from high-growth acquirer to cash-generative operator—offers a blueprint, not an endpoint.